Iran Overview

Iran also called Persia, and officially the Islamic Republic of Iran, is a country in Western Asia. With 83 million inhabitants, Iran is the world's 18th most populous country. Its territory spans 1,648,195 km2 (636,372 sq mi), making it the second largest country in the Middle East and the 17th largest in the world. Iran is bordered to the northwest by Armenia and Azerbaijan, to the north by the Caspian Sea, to the northeast by Turkmenistan, to the east by Afghanistan and Pakistan, to the south by the Persian Gulf and the Gulf of Oman, and to the west by Turkey and Iraq. Its central location in Eurasia and Western Asia, and its proximity to the Strait of Hormuz, give it geostrategic importance.

Tehran is the political and economic center of Iran, and the largest and most populous city in Western Asia with more than 8.8 million residents in the city and 15 million in the larger metropolitan area

Iran is a founding member of the UN, ECO, OIC, and OPEC. It is a major regional and middle power, and its large reserves of fossil fuels including the world's largest natural gas supply and the 4th largest proven oil reserves exert considerable influence in international energy security and the world economy.

Iran Political Systems

The country's rich cultural legacy is reflected in part by its 24 UNESCO World Heritage Sites, the 3rd largest number in Asia and 10th largest in the world. Historically a multi-ethnic country, Iran remains a pluralistic society comprising numerous ethnic, linguistic, and religious groups, the largest being Persians, Azeris, Kurds, Mazandaranis and Lurs.

Iran's political system has elements of a presidential democracy with a theocracy governed by an autocratic "Supreme Leader”. The Supreme Leader of Iran is the head of state and highest ranking political and religious authority which is above the President. The armed forces, judicial system, state television, and some of key governmental organizations are under the control of the Supreme Leader.

Iran is a republic in which the president, parliament and judicial system share powers reserved to the national government, according to its Constitution. The politics of Iran take place in a framework that officially combines elements of theocracy and presidential democracy. The December 1979 constitution, and its 1989 amendment, define the political, economic, and social order of the Islamic Republic of Iran, declaring that Shia Islam is Iran's official religion.

Iran has a democratically elected president, a parliament, an Assembly of Experts which elects the Supreme Leader, and local councils. According to the constitution, all candidates running for these positions must be vetted by the Guardian Council before being elected.

Iran Economy

Iran’s Gross Domestic Product (GDP) in 2019/20 is estimated at US$463 billion. With a population of 83 million people, Iran’s economy is characterized by the hydrocarbon, agriculture, and services sectors, as well as a noticeable state presence in manufacturing and financial services. Iran ranks second in the world in natural gas reserves and fourth in proven crude oil reserves. Economic activity and government revenues depend to a large extent on oil revenues and therefore remain volatile.

The Iranian authorities have adopted a comprehensive strategy encompassing the market-based reforms reflected in the government’s 20-year vision and its sixth development plan for the full five-year period from 2016/17 to 2021/22. The plan is composed of three pillars, namely, the development of a resilient economy, progress in science and technology, and the promotion of cultural excellence. On the economic front, the development plan envisages an annual economic growth rate of 8% and the reform of state-owned enterprises and the financial and banking sectors. The allocation and management of oil revenues are among the government’s main priorities.

Economy after sanctions

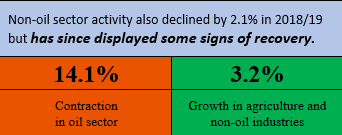

After a 4.7% contraction of GDP in 2018/19, GDP declined further by 7.6% (yoy) in the first nine months of 2019/20 due to the contraction of the oil sector and weak domestic demand. The oil sector contracted by 14.1% in 2018/19 following the reintroduction of US sanctions in May 2018, contributing the most to overall negative growth. Non-oil sector activity also declined by 2.1% in 2018/19 but has since displayed some signs of recovery. Between April and December 2019, agriculture and non-oil industries grew by 3.2% and 2% (year-on-year), respectively, while value-added services edged down.

The unemployment rate remains high, at 10.6% as of October to December 2019, though it showed improvement compared to the same period the previous year (11.8%).

Real exports of goods and services contracted by 13.6%after a small growth of 1.8% in the previous year. Real imports contracted sharply by 38.3% due to restrictions on the import of non-essential goods aimed at controlling the pressure on foreign exchange reserves.

Since the attempted unification of the official and parallel exchange rates in April 2018, the economy has been effectively operating under a multiple exchange rate system. In the parallel market, the rial has depreciated more moderately against the dollar in 2019/20 after recovering from a strong decline in mid-2018 due to a surge in speculative foreign exchange demand. Inflation started a gradual decline from a peak of 52% (yoy) in May 2019 to reach 22% in March 2020 as the base effect of the earlier depreciation period declined.

Higher import prices and trade restrictions are likely to keep inflation above 20 percent in the coming years. Despite the rial’s depreciation and a large drop in imports, the reduction in oil exports is expected to weigh more heavily on the current account balance than the earlier episode of sanctions, as oil prices are much lower than they were in 2012/13 to 2013/14. The stagnating trajectory of the economy is also likely to put further pressure on labor market dynamics and job creation.

In the medium term, the economy is set to experience a slow recovery with oil exports expected to remain at historic lows and non-oil activity remaining subdued. Facing additional exogenous shocks—including the COVID-19 outbreak in 2020—GDP is expected to further contract in 2020/21. Economic growth between 2020/21 and 2022/23 is expected to remain weak between 2020/21 and 2022/23, experiencing a small pickup in exports and consumption on the demand side and the industry sector on the supply side in the outer years.